.svg)

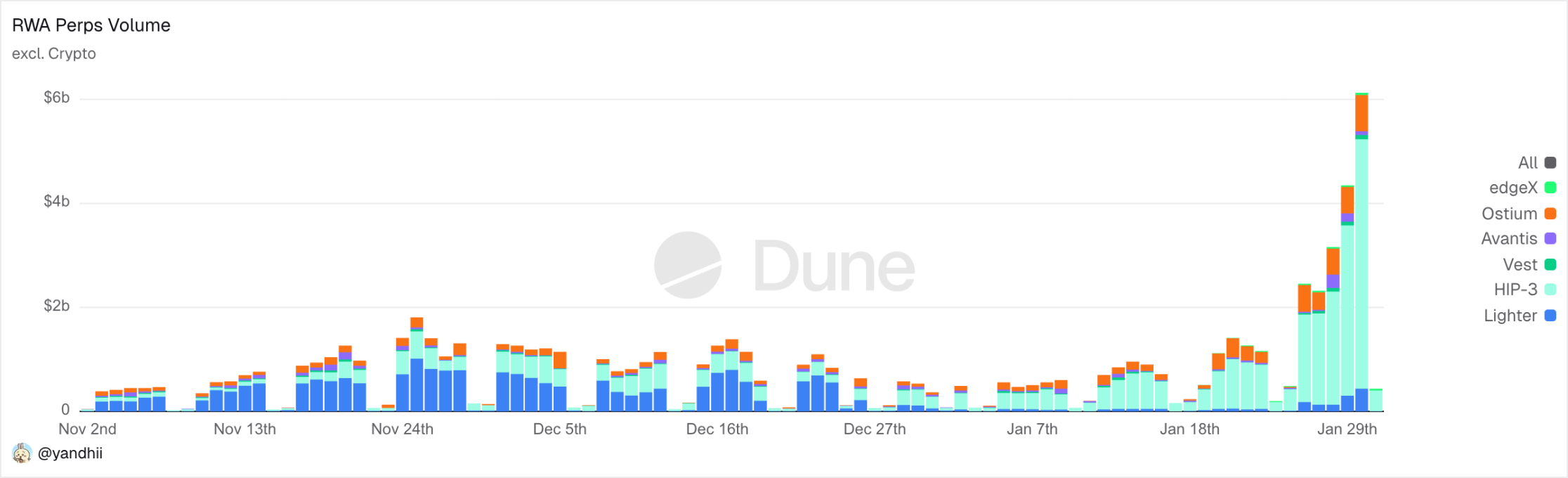

In late January 2026, RWA perpetual volumes exceeded $2B per day on decentralized platforms alone, with Hyperliquid and TradeXYZ driving the majority of activity. The commodity surge that week demonstrated the infrastructure's capacity to handle multi-billion-dollar volume spikes—and this is only the beginning.

The chart above tracks daily RWA perpetual volume across decentralized platforms, excluding crypto-native pairs. The late January spike reflects the commodity surge discussed later in this article, with daily volumes briefly exceeding $4B.

Based on Kappa Lab's market intelligence across major platforms as of January 2026, the commodity perpetual market significantly outpaces equity RWAs in daily volume. Gold and Silver perpetuals dominate this landscape, representing the vast majority of commodity perpetual activity, with TradeXYZ and Binance together accounting for roughly 80% of total commodity perpetual trading. While platforms have introduced Copper, Platinum, Natural Gas, and WTI Oil perpetuals, precious metals remain the most mature and liquid RWA markets on-chain—making them an ideal lens for understanding how 24/7 infrastructure interacts with traditional market schedules.

While the infrastructure is fully on-chain and operates 24/7, liquidity still largely adheres to traditional trading hours. A detailed order book depth analysis reveals a clear pattern: liquidity declines materially during traditional market closures, despite these markets trading 24/7.

This reflects the reality that both market makers and end clients remain anchored to legacy trading hours—for now.

Liquidity Behavior Across Time

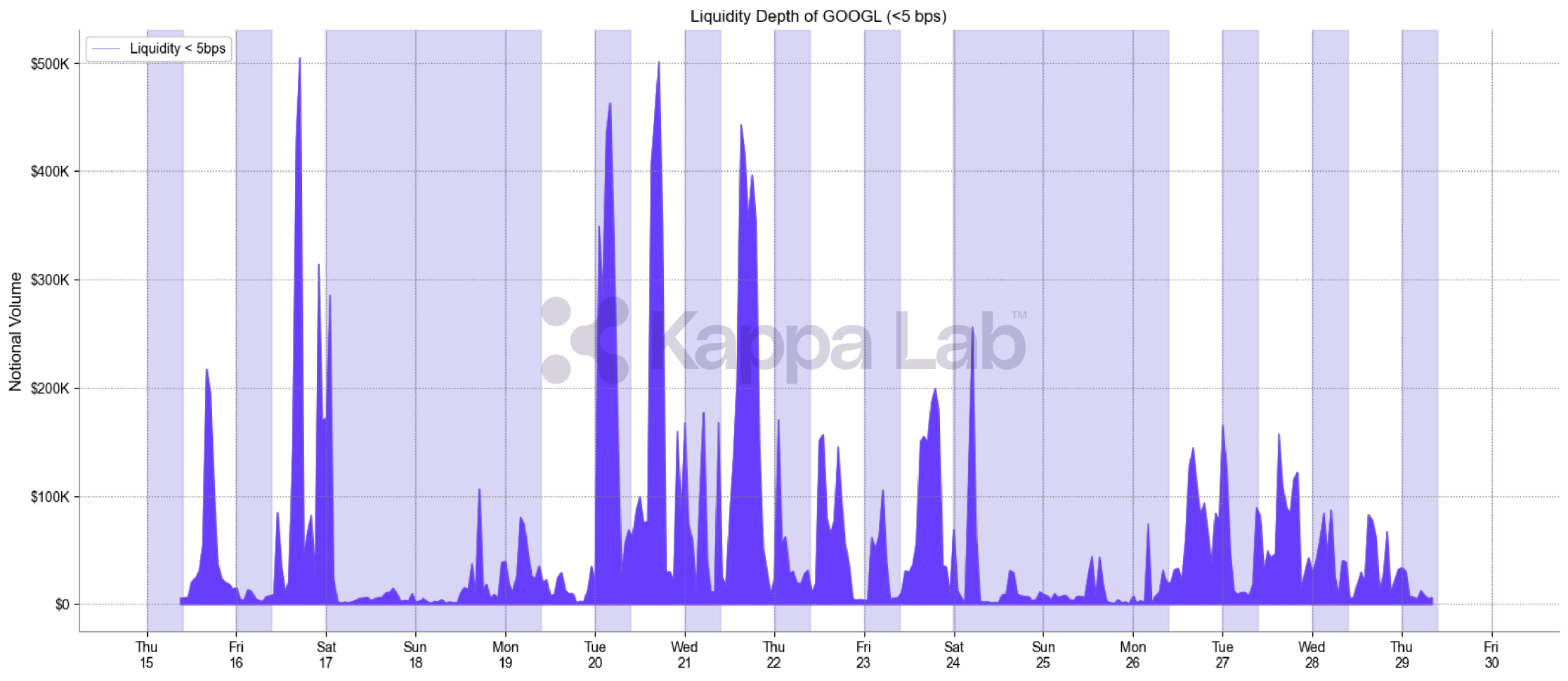

Order book depth for GOOGL perpetuals on TradeXYZ was analyzed from January 15-29, 2026. The analysis tracks liquidity patterns at two bid-ask spread thresholds: under 5 bps and under 20 bps.

These measurements were tracked across distinct time windows:

- Normal U.S. Trading Hours (9:30 AM–4:00 PM ET): Order book depth is stable and well distributed. Market makers consistently quote tight spreads with healthy aggregate size, reaching peaks of $500K at <5 bps and $1M at <20 bps.

- After-Hours Trading (4:00 PM–8:00 PM ET): Liquidity remains available but at materially lower levels. Participation narrows, with reduced order sizes and thinner depth.

- Extended Hours (24/5 via select brokers): On-chain perpetual liquidity improves modestly relative to standard after-hours trading but remains below levels observed during regular market hours. Coverage is limited to weekdays (24/5 rather than 24/7), providing a partial bridge without fully closing the off-hours liquidity gap.

- Weekends: Order book depth contracts sharply. Available liquidity frequently approaches zero, with only limited participation at significantly reduced sizing.

Periods highlighted in light purple correspond to U.S. market closures, including after-hours sessions and weekends. During these intervals, liquidity systematically withdraws from the order book. This behavior persists regardless of whether liquidity is measured at tight or wide bid-ask spreads. While the magnitude varies, the direction remains unchanged.

A notable observation: liquidity depth looks nearly identical beyond the 20 bps threshold. Most available liquidity is concentrated within tight spreads, suggesting limited market maker diversity—primarily active participants quoting tight rather than passive liquidity resting at wider levels. This is positive for execution quality during market hours, but it also explains the sharp collapse in depth during off-hours: when active market makers step back, there is no backup liquidity at wider spreads to cushion the withdrawal.

Asset Type Matters: Commodities Show Greater Resilience

While the structural constraints described above affect all RWA perpetuals, the severity varies significantly by asset class. Commodity perpetuals demonstrate materially stronger weekend liquidity compared to equity perpetuals.

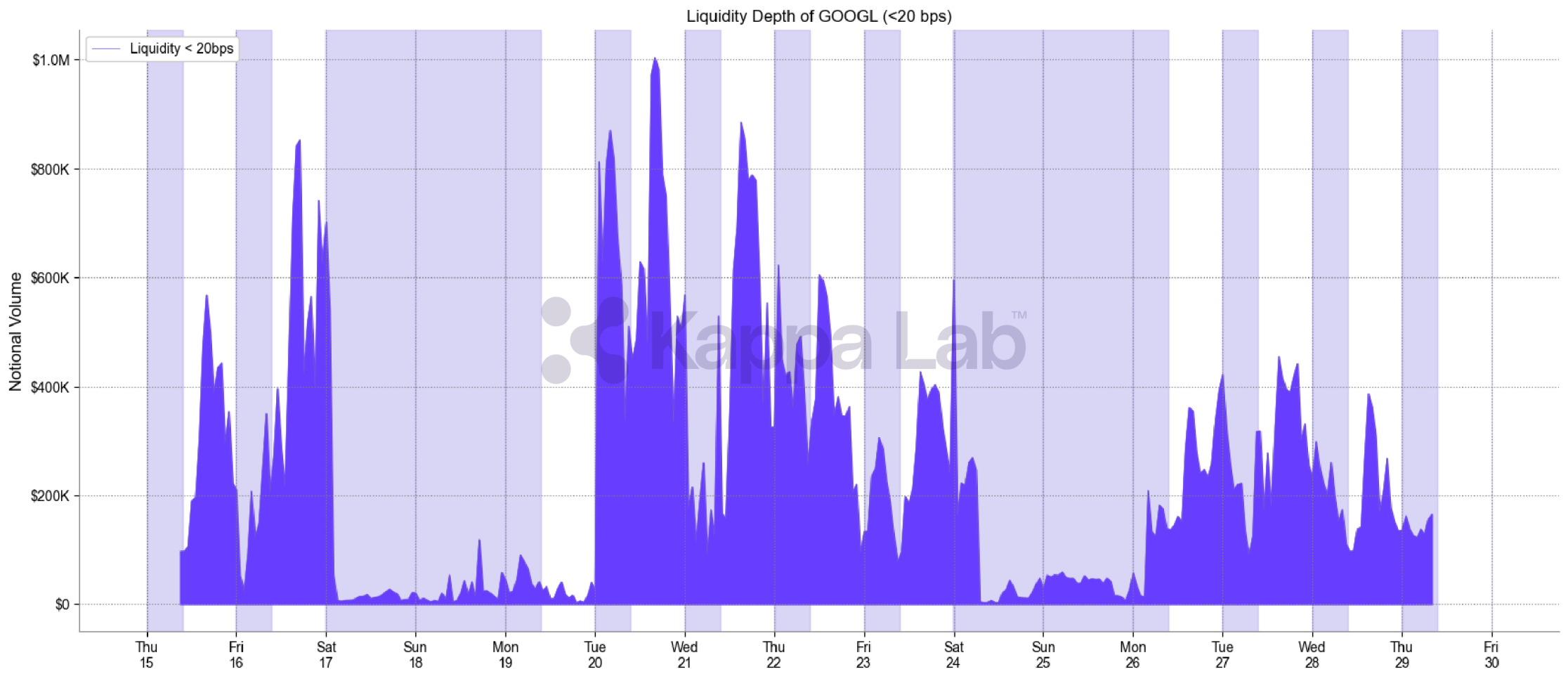

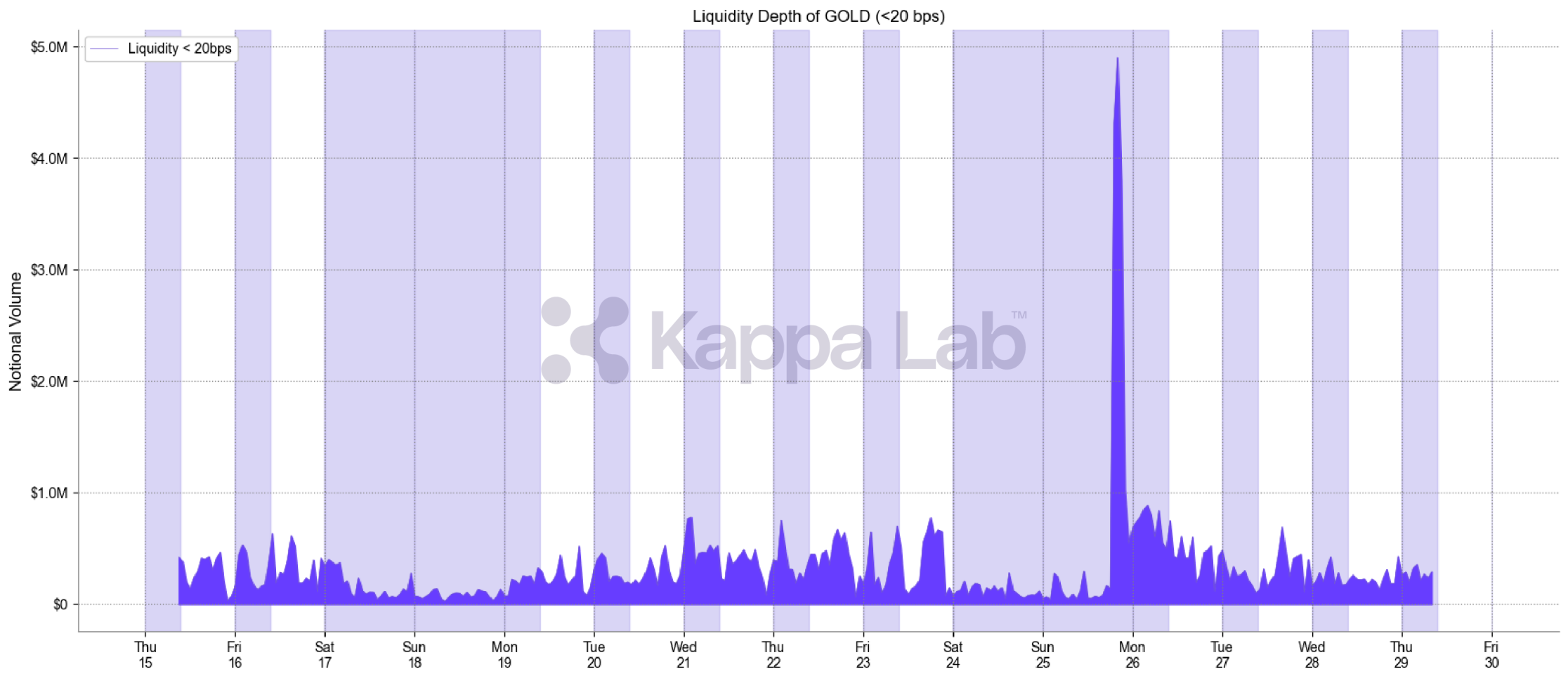

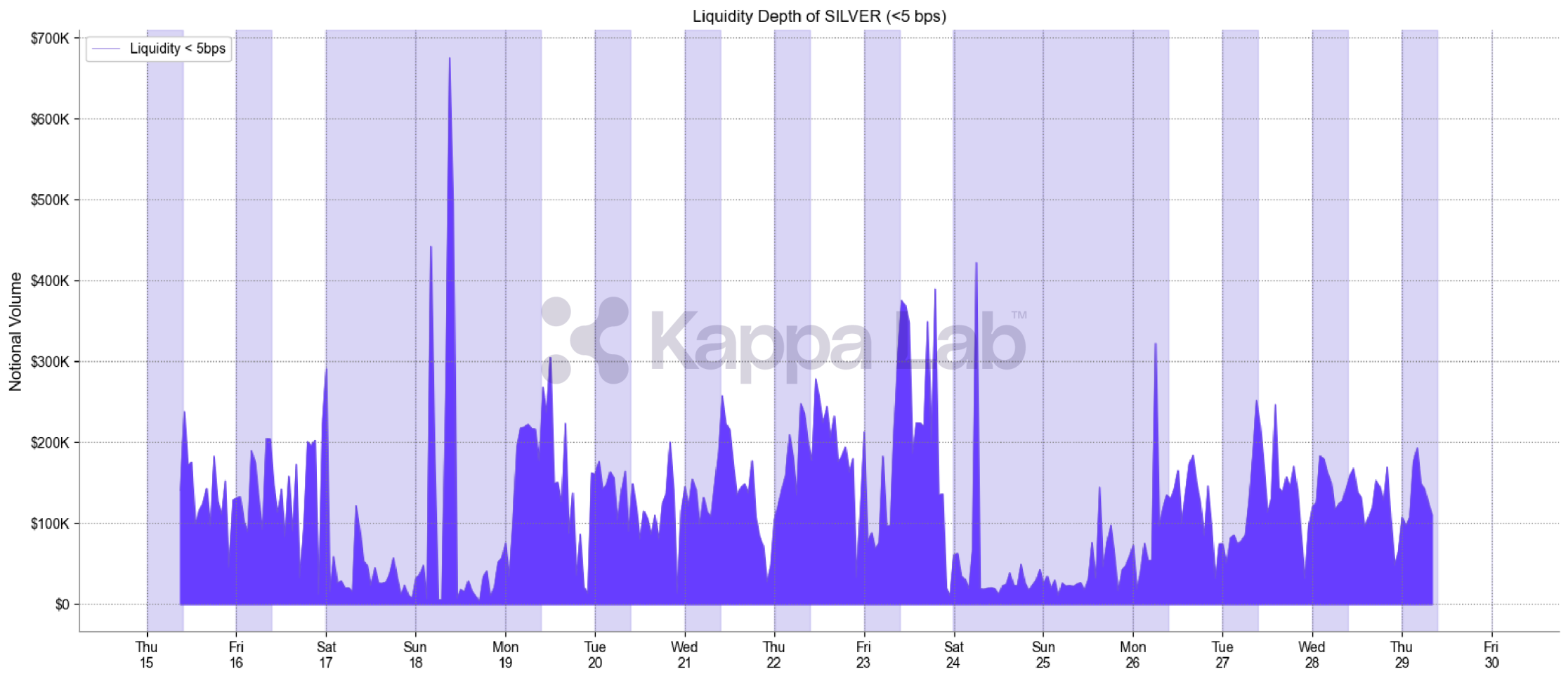

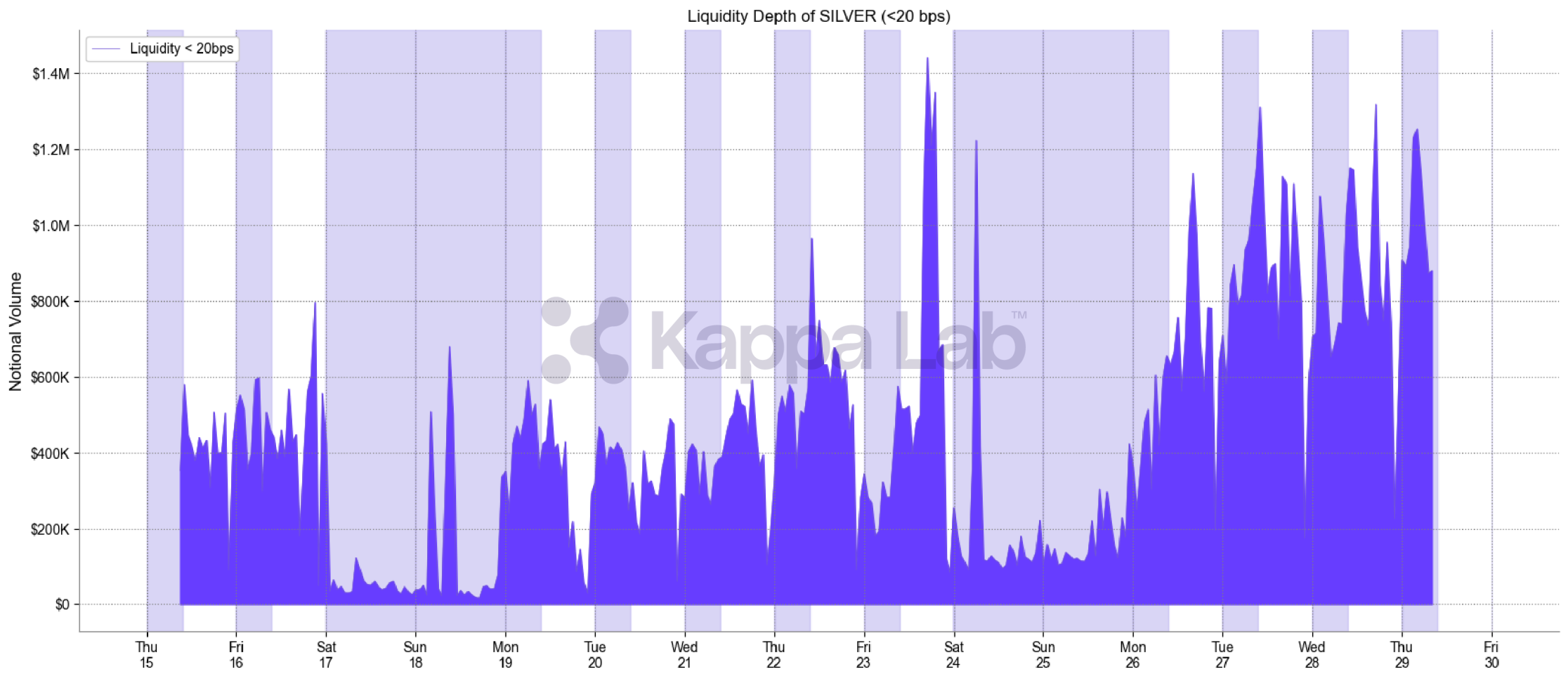

Analysis of Gold and Silver perpetuals on TradeXYZ from January 15-29, 2026, reveals a different liquidity profile than equities. While the same pattern of weekend contraction appears, commodity markets maintain substantially higher depth during off-hours periods.

Market hours for gold and silver:

- Opening hours: Sunday 6:00 PM ET to Friday 5:00 PM ET

- Daily maintenance window: 5:00 PM to 6:00 PM ET, Monday through Thursday

- Spot gold and silver trading also follow CME holiday closures

The charts below track order book depth for Gold perpetuals on TradeXYZ at two bid-ask spread levels: tight (<5 bps) and medium (<20 bps).

Silver perpetuals show similar patterns across the same spread thresholds:

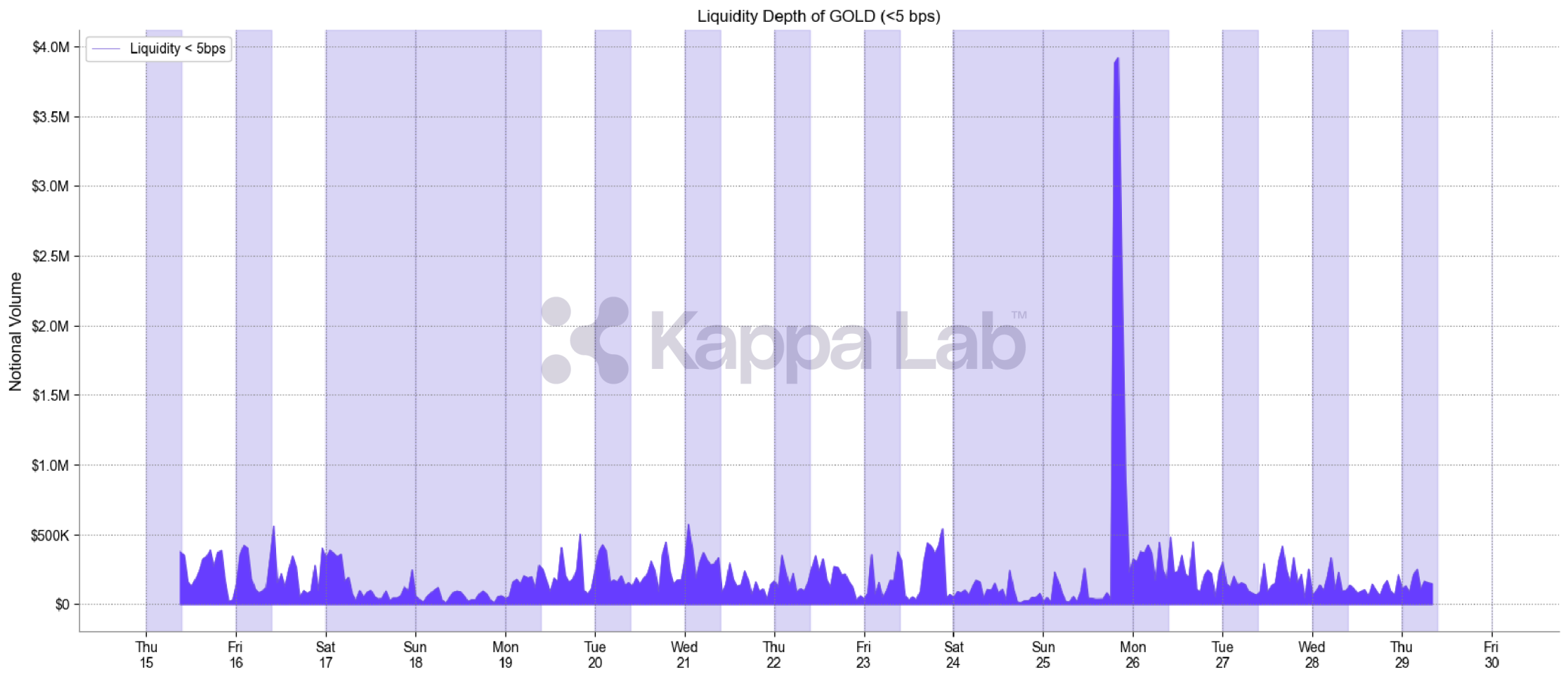

Context: Record Volatility Week

The liquidity data shown for Gold and Silver (January 15-29, 2026) captured a historic week in commodity markets. On Monday, January 26, gold breached $5,000 per ounce for the first time, reaching an all-time high of $5,102, while silver hit a record $117.69.

CME Group reported a single-day record of 3.3 million contracts traded across its metals complex, surpassing the previous record set in October 2025.

The surge was driven by multiple factors: intensifying geopolitical tensions (Greenland, Venezuela, Middle East), significant dollar weakness, record ETF inflows, and anticipation around the Federal Reserve's January 27-28 policy meeting. Silver's rally was further amplified by industrial demand tied to the AI infrastructure buildout.

The massive liquidity spike visible on Monday, January 26 in the Gold chart—reaching $3.9M at <5 bps—reflects this macro volatility meeting 24/7 on-chain infrastructure. When genuine price action and trading flow arrive, perpetual markets can support substantial depth even during periods when traditional markets are transitioning from weekend closures back to active trading.

Crypto-Native Hedging Infrastructure

The availability of hedging venues within the crypto ecosystem has been critical to commodity perpetual liquidity growth. Binance launched gold perpetuals (XAUUSDT) on January 5, 2026, and silver perpetuals (XAGUSDT) on January 7, 2026, providing crypto-native market makers with accessible hedging infrastructure using their existing operational stack—Binance accounts, stablecoin settlement, and established API connections—rather than navigating traditional broker-dealer relationships and fiat settlement cycles. The availability of liquid hedging venues within the crypto ecosystem removes a major operational barrier that would otherwise force market makers to step back during off-hours.

Key Differences Across Asset Classes

Gold perpetuals maintained $300K-$500K in depth during regular hours at <5 bps, with the January 26 volatility spike reaching $3.9M. Even on weekends, Gold retained meaningful liquidity rather than collapsing to zero. Silver showed similar resilience, maintaining $150K-$300K during regular hours at <5 bps, with notable weekend activity—including a spike to ~$680K on Sunday, January 18.

By contrast, GOOGL peaked at similar levels (~$500K at <5 bps) during regular trading hours but saw lower depth on weekends.

Peak weekday liquidity for commodities at <20 bps reached $5M+ (Gold) and $1.4M+ (Silver), materially higher than equity perpetuals.

Why Commodities Behave Differently:

- Nearly Continuous Traditional Markets: COMEX trades Sunday evening through Friday afternoon (23/6 coverage), providing pricing references and hedging venues during most weekend hours. Equity markets remain fully closed on weekends.

- Higher Organic Weekend Flow: Commodities attract more genuine trading activity during off-hours as global macro events unfold continuously. This creates stronger economic incentives for market makers to maintain quotes even during internal pricing sessions.

- Better Hedging Infrastructure: Commodity futures markets offer superior 24/7 hedging capabilities compared to equity markets, reducing the gap risk that forces equity market makers to pull liquidity.

Binance only introduced its first equity perpetual market on January 28, 2026, highlighting the maturity gap between commodity and equity RWA perpetuals in terms of available hedging infrastructure within the crypto ecosystem.

The structural constraints described below apply across all RWA perpetuals, but asset classes with more continuous traditional market infrastructure demonstrate that the 24/7 paradox can be partially bridged when underlying pricing and hedging venues operate near-continuously.

Two Structural Constraints

1. Pricing Infrastructure

Market makers quote around a fair value derived from external reference prices.

When U.S. equity markets are open, that reference is continuously refreshed through active price discovery. When they close, price discovery slows materially or halts altogether. While futures and derivatives markets extend coverage into overnight sessions, weekends remain largely inactive. In the absence of live reference prices, liquidity providers must either widen spreads to compensate for increased uncertainty or reduce quoting activity altogether.

During active trading sessions, platforms ingest price data from institutional liquidity providers via partners such as Pyth Network. Pyth Lazer, purpose-built for latency-sensitive applications like perpetual futures, delivers ultra-low-latency price feeds with configurable update frequencies as fast as one millisecond. These sub-second updates support real-time price discovery when underlying markets are active.

This is not a failure of on-chain infrastructure. It reflects the fundamental reality that the underlying asset does not trade continuously. Oracles can transmit available information with minimal delay; they cannot create price discovery where none exists.

2. Hedging Facilities

Professional liquidity provision is typically structured to be delta-neutral, with exposure actively managed through hedging in the underlying market or in closely correlated instruments.

When traditional venues close, those hedging channels effectively disappear. Carrying unhedged equity exposure through non-trading periods introduces gap risk driven by discrete news events rather than continuous intraday price dynamics. For most market makers, this risk profile is difficult to justify within standard spread and inventory economics.

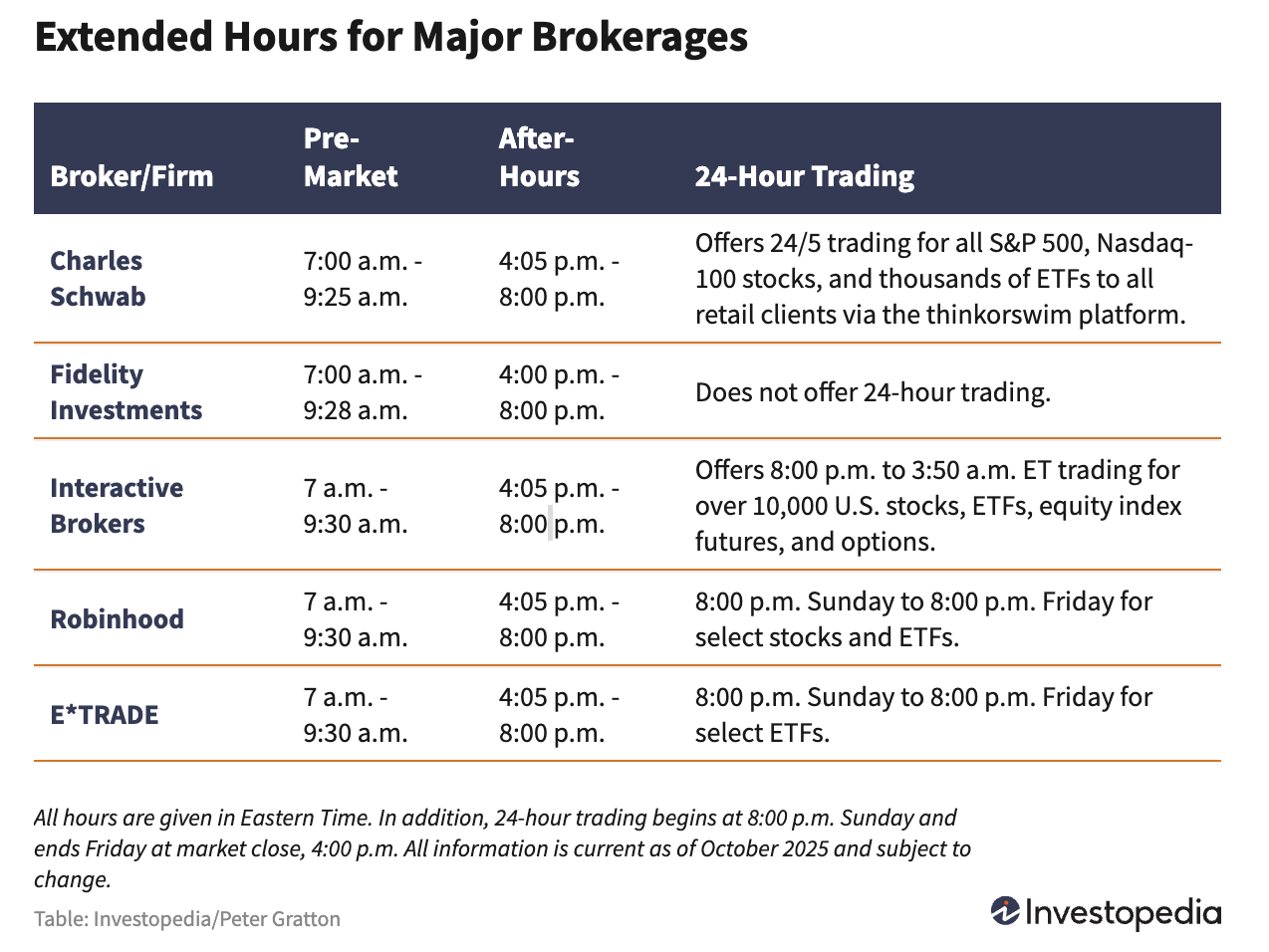

Although some brokers have extended trading hours, effective hedging availability remains constrained in both depth and continuity:

Even with extended-hours offerings from select brokers, coverage remains limited to weekdays. Charles Schwab offers 24/5 trading for all S&P 500, Nasdaq-100, and Dow 30 stocks, plus over 600 ETFs, while Interactive Brokers extends trading to approximately 3:50 a.m. ET for more than 10,000 equities. However, all traditional venues remain closed over weekends.

As a result, liquidity providers typically step back during non-trading periods, and order book depth contracts materially, despite the perpetual market's technical ability to operate continuously.

A Hybrid Market Structure

RWA perpetuals operate at the intersection of two distinct systems. The execution layer is crypto-native and continuously available, while the pricing and risk layers remain fundamentally anchored to traditional market schedules.

Some venues are experimenting with mechanisms to smooth this discontinuity, including internal price formation during off-hours and hybrid oracle frameworks that adapt their inputs when external reference markets are inactive.

Internal Price Discovery

TradeXYZ implements a continuous-time exponentially weighted moving average (EMA) mechanism for internal pricing when external data becomes unavailable. The system calculates an impact price difference (IPD) based on the average execution prices for configured notional amounts on both sides of the order book. The oracle then advances incrementally using a one-hour time constant, adjusting the previous oracle price by a fraction of this IPD.

This internal mechanism initializes from the last available external price when markets close. When external inputs resume, the oracle reverts to externally derived spot prices on the next update. The approach creates continuity across non-trading periods but inherits the order book's own liquidity state, which itself degrades during off-hours.

These mechanisms can reduce discontinuities, but they do not remove the underlying dependency on traditional markets.

Insights from Market Making RWA Perpetuals

Infrastructure Gaps

Crypto infrastructure and traditional financial infrastructure remain fundamentally different. Systems built and optimized for venues like Binance and Hyperliquid face material challenges when interfacing with traditional equity markets.

Broker-dealer relationships operate on different settlement cycles. Fee structures shift from basis points on notional to per-contract models. Trading hours are not continuous. Clearing and custody frameworks don't map cleanly to crypto-native operations. These frictions create operational complexity that goes beyond simply connecting to an API.

Market Structure Opportunity

Despite these challenges, edge exists. Current participants largely employ basic setups. Many market makers run unhedged positions or use correlation-based strategies that assume stable relationships between certain equities and indices.

Whether these approaches scale as more sophisticated participants enter remains an open question. As flow grows and sharper traders arrive, strategies that work in thin, retail-dominated markets may face different dynamics.

Real Flow Patterns

Beyond farmers crossing the top of book, these markets show genuine price action. Participants use RWA perpetuals for portfolio allocation, directional speculation, and price discovery. The flow is real, even if volumes remain relatively small for equities compared to the dominant commodity perpetual markets.

This creates an opportunity for liquidity providers who can navigate the infrastructure challenges and operate across both traditional and crypto market structures. At Kappa Lab, we've built systems to bridge these frameworks, providing institutional-grade liquidity where the two ecosystems intersect.

Implications for Market Design

True 24/7 liquidity requires more than continuous matching engines. It requires continuous pricing references and hedging venues.

As open interest in RWA perpetuals continues to grow, off-hours liquidity becomes a structural consideration rather than a temporary inefficiency. The analysis across asset classes demonstrates that when underlying traditional markets operate near-continuously—as with commodities—on-chain perpetuals can maintain materially stronger weekend depth.

Until pricing and hedging infrastructure evolve beyond traditional schedules for equities, these markets are likely to continue reflecting the hours of the assets they reference, even if trading never technically stops. Commodity perpetuals point toward what's possible when traditional market infrastructure provides better coverage.

The infrastructure is ready, but the ecosystem supporting it is still catching up. As these markets continue to grow, understanding these liquidity patterns will be critical for anyone building or trading on-chain.

Your Liquidity?

.svg)

.svg)

.svg)

.svg)

Kappa Lab Capital DMCC is a proprietary trading firm registered in Dubai, UAE. It operates under a No Objection Confirmation (NOC) from the Virtual Asset Regulatory Authority (VARA).

The information on this website is not directed at nor intended for distribution to, or use by, any person resident in any country or jurisdiction where such distribution or use would be contrary to local law or regulation. The content on this website is for informational purposes only and should not be considered an offer or solicitation to engage in any financial activity.